Uh, oh:

CNNMoney reports:

"Under these circumstances, to start off the season in this fashion is truly amazing and is a testament to the resiliency of the American consumer, and undeniably proves a willingness to spend," Martin said in a statement.

Uh, oh:

CNNMoney reports:

"Under these circumstances, to start off the season in this fashion is truly amazing and is a testament to the resiliency of the American consumer, and undeniably proves a willingness to spend," Martin said in a statement.

"Where are we in the cycle?"

"Goldilocks has eaten and slept and the bears have just come home."

Meanwhile, real disposable income was up on this morning's dipstick, so ...

NO SUCH THING AS A STUPID LOAN OR A SILLY LENDER

If you missed it, they are all excited over at HUD about a new form, that has no enforcement mechanism and won't be required until 2010. (It's still a big deal, maybe a break in a multi-decade log-jam, even).

Meanwhile, everyone, Left and Right, is agreed that some form of debt-counseling helps improve mortgage loan performance. We voted federal money for it, in the past year, maybe twice.

Still, no one appears to study the affect of education (or jail?) on ... those doing the lending. It's an abstract we prefer to call 'structural market failure', I guess, related to 'mis-aligned' incentives. No culpability there.

The knee-jerk free-marketeers seem to believe that the appropriate penalty for lender silliness is their own bankruptcy, not discharge of their poorly conceived loans.

Sampler from some of the recent financial reports for financial institutions. Sometimes, things just jump off the page at you:

Sampler from some of the recent financial reports for financial institutions. Sometimes, things just jump off the page at you:

(1) The Sub-Prime Group (SPG) exposures became fully integrated into VAR during the first quarter of 2008. As a result, September 30, 2008 and third quarter 2008 average VAR increased by approximately $60 million and $73 million, respectively. June 30, 2008 and second quarter 2008 VAR increased by approximately $95 million and $135 million, respectively.

(1) The FRB granted interim capital relief for the impact of adopting SFAS 158, “Employer’s Accounting for Defined Benefit Pensions and Other Postretirement Benefits” (SFAS 158), at December 31, 2006.

The claims are for breaches of the duty of care, breach of fiduciary duty, waste, insider trading, fraud, gross mismanagement, violations of the Sarbanes-Oxley Act of 2002, and unjust enrichment.

Derivative contracts with a financing element, net | YTD 2008 73 | YTD 2007 3,887 |

This new ABS lending program from the Treasury/Fed is quite a powerful construct, providing 'levered financing' to the market. Woo-hoo!

This term-financing for up to a year for a variety of initial asset types, subject to a (one-year?) price-volatility haircut. The collateral must be "AAA", highest quality. In addition to the price/market-risk haircut, the Treasury then backstops the Fed with an equity pool, for the credit risk.

Two things I don't like, based on a quick first-read.

- 'AAA' may not be the part of the market that needs the most help. I'd like to see a broader range of collateral. All qualities may need help, to the extent the market is shut down, but still.

- The Treasury ought not to be the one managing the collateral, unless it intends to immediately enter into a forward purchase agreement with someone in the marketplace (and take a residual risk to lubricate the deal, maybe).

The Fed using it's balance sheet during crisis is just fine. However, with this latest construct, the Government looks like it is too much both the supply and the demand for funds. Of course, it's just $200 billion, so no need to wring hands over it, either.

"Dual-action" may be fine to address a blip in a market or smooth things over, in a market that isn't huge. It may even be a powerful "can-do" in a near deflationary environment.

But, on face, it doesn't seem a sound recipe for the long-term or for much larger asset classes, like commercial real-estate or private-label RMBS (nor does 1-yr term financing, given the duration of the underlying collateral of those instruments)

...until agency spreads blow out, no doubt. Just another lame attempt by the outgoing administration to hand-tie the nation and the new administration.

There are days that I think the GOP no longer care about the finances of the Republic - even its homeowners - and would just assume see it go through "bankruptcy", just like they want for GM and every other homeowner who gets a foreclosure notice.

It bears reminding, I guess, that we are a nation of people, not merely cash flows and assets:

So, now that the McCain camp which tried to use this same “Fannie/Freddie did it” fairy tale in its anti-Obama campaign—is history, as is most of Fannie and Freddie--what are the Republicans going to dredge up to in an effort to sanitize their regulatory shortcomings and, once again, blame Fannie Mae and Freddie Mac?

Most observers point to the seminal actions by Mudd and Syron, respectively, to purchase large amounts of toxic Alt A and private label subprime securities (PLS) in 2006 and 2007, as the major red ink causes.

But, almost as important, is the fact that virtually every aspect of the two mortgage companies business was presided over and blessed by their former regulator the Office of Housing Enterprise Oversight (OFHEO), following the May, 2006 consent agreements both companies signed with OFHEO. From that point on, the regulatory agency had their own employees in both companies every business day of the week reviewing all transactions and decisions.

If the former GSE managements made bad business calls, what’s that say about the OFHEO staff who shared in their meetings and machinations?

This next Waxman hearing should be fun to watch as the Committee GOP has to perforce blame other Republicans for mortgage misfeasance or malfeasance!

THE PRICE OF INFLATION/DISINFLATION/DEFLATION UNCERTAINTY

Robert Barro points out that there may be a current, sizable deflation risk premium, just as there was once an inflation-risk premium incorporated in the observed yields (although some thought that had since passed, with the ability to use products to manage inflation risks...).

Uncertainty about how best to use these expectational variables has kept me from updating the rates chart, for now. They are projecting maybe five years of deflation. [!]. It's possible that the structure of the TIPS offering has some technical impact, not just the liquidity.

Separately, perhaps one of the NIPA pros can explain why the price indexes for Q3 GDP were rising for line items like "Gasoline, fuel oil, and other energy goods" and how the consumption deflator seems... so large.

TARP INFUSIONS ONLY INDIRECTLY RAISE COMMON STOCK PRICES

There is this post over at Brad DeLongs, with a high level view of what happened to Citi.

Here is another stylized view, Citi by the numbers:

At the end of 2006, Citibank had just under $90 billion in tangible, common shareholder equity. That would be about $18/share. The market liked Citi enough to pay up almost 2.7 times tangible book for a common share.

Twenty-one months later, by the end of the third quarter of 2008, Citibank had recognized $32.2 billion in credit losses and provisions for losses, earning 3.6 billion in 2007 and losing about $10 billion in 2008 (so far).

Tangible book value of common was $68.8 billion or about $12.60/shr and the market was paying up as little as $4-$6/shr, implying significant further loses. If those loses were in the range of $33 billion, it would imply a valuation of just 1.0 times tangible book (based on my guesstimates for earnings over the next 18 months).

Yes, that's a big drop in the premium paid. The stock is "washing out", as the pros say.

n.b. TARP "infusions" do not make the stock price go up or boost the capital stake for common holders, just for the firm as a whole. I'm guessing this may be creating a great deal of confusion in the punditocracy, because it looks like the TARP isn't "doing anything", because people are looking at the common stock price and asking, "why is it going down, not up, after TARP?"

See also, The Bankless Rally

WHAT'S THE BREAKDOWN FOR HOW CITI 'LOST' ITS MONEY SO FAR?

I don't have these figures in detail. The company did offer up this high-level summary, during it's "Townhall Meeting". "LLR" are loan-loss reserves. "S&B" is 'Securities and Banking', which, for them, includes structured products, trading, private equity, investment banking, hedge funds, and a lot more.

FIND YOUR INNER VULTURE - THE TIME IS RIPE

The service companies arise:

Colliers Abood Wood-Fay Launches Distressed Property Services Group

Published: November 20, 2008

Miami--Colliers Abood Wood-Fay recently launched its Distressed Property Services Group. The group brings together an integrated team of resources, disciplines and professionals with over 75 years combined experience in managing distressed assets in inflationary or recessionary markets.

They are focused on some stupid meme about taxes on the wealthy?

We're bailing out the entire financial system, and this is what is topic number one?

The market is selling off? As if they have never heard about sell the news? (*eyes roll*)

Very impressive.

SAVING PRIVATE RYAN, ...ER, CITIBANK

Our Nation's quick-draw team has ... had another bailout weekend. Citigroup is the patient on the table, five-days after they started a free-fall. The deal is the deal, improvised or not. I don't think you need to take-up 90% of the residual to make a good re-insurance market, but other (more informed) opinions could be had on that. It's a noteworthy point, especially because one may want to repeat this guarantee immediately at the next target (and there will be one, right?). I also think that the government should have left some of the tail probability on the table, taking just a "slice" not the whole enchilada. Last, a back-of-the-envelop, 10% haircut seems ... so yesterday, compared to the valuation technologies available, presently. Also, I guess Wilbur Ross, a lighthouse of the free-marketeers, wasn't available...

The deal is the deal, improvised or not. I don't think you need to take-up 90% of the residual to make a good re-insurance market, but other (more informed) opinions could be had on that. It's a noteworthy point, especially because one may want to repeat this guarantee immediately at the next target (and there will be one, right?). I also think that the government should have left some of the tail probability on the table, taking just a "slice" not the whole enchilada. Last, a back-of-the-envelop, 10% haircut seems ... so yesterday, compared to the valuation technologies available, presently. Also, I guess Wilbur Ross, a lighthouse of the free-marketeers, wasn't available...

The markets will likely cheer the result, in a modest way, but will wonder if we still have moved from weekend-solutions to a comprehensive solution that was sought by "enacting TARP".

MEANWHILE, IN THE REAL ECONOMY

Meanwhile, the worst number from last week was the yield on long-term Treasuries.

That was no panic buying (I don't think). The market has clearly started to lose confidence in the direction of the real U.S. economy. Chief culprits are the Bush-Paulson abdicating their leadership and a lack of a plan to address the bad-asset problem, right at the source - foreclosures, real-estate price declines, and, now, weak economic activity.

WHEN ALL THE SHOES HAVE DROPPED ...

The diagrams of a "bad-asset cycle" suggest, conventionally, that economic stimulus will "break the cycle", even if I thought that addressing the bad-asset problem (the value of home collateral) directly would have been a good first "stimulus" step.

So far, our reactive policy seems unable to get ahead of the curve. We haven't stopped any market from "breaking", that I can think of. To paraphrase Galbraith, "the key feature of the panic was that it kept getting under-estimated [until the system was so weak that antibiotics wouldn't work]."

Snarking aside, we can (and must) track the shoes in the cycle:

On deck:

For those who keep asking about a market bottom, Paul Kedrosky wonders aloud about whether the worst is past.

The lack of systematic, government-mandated and collected statistics on the structure of the mortgage loan market appears to be a running theme in how the uncertainty keeps going, and going, and going. (There may be some that I just do not know about).

Among the things I haven't seen systematically outlined:

So, Tim, how are you at insurance? (Do we dare to ask Paulson & Co.?)

I mean, you can "TARP" Citi if you need to, but, in the words of MetLife, "Who's gonna pay for this mess?" (and it *must* be attended to, maybe even this weekend):

The Hartford Group and Lincoln Life, 5-days of gruesome giddy-up

Chart of yester-jour was AMBAC, up 86%:

Ambac Assurance Corp, Ambac's main unit, paid $1 billion to get out of four contracts it had written to guarantee collateralized debt obligations, reducing the bond insurer's liabilities. It said the terminations would allow it to reduce reserves set aside for market losses on these guarantees. - Reuters

S&P downgraded the senior debt of Ambac Financial (ABK) to BBB from A. It also cut Ambac Assurance Corp., the bond insurance subsidiary, to A from AA. The outlook is negative.-SmartMoney

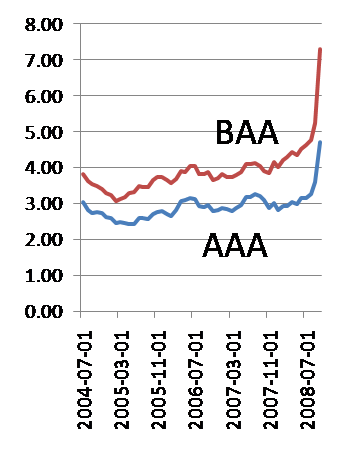

Using the Fed series for corporate rates, less y/y CPI (not necessarily the best, but the easiest), I have a somewhat different picture than PK has for real rates.

In fact, it is sufficiently different that one can question the read that these levels are due to a factoring in of a collapse of the system. Rather, they look a lot more like the "Greenspan conundrum" has been canceled, and the US is ...er, back to where it used to be, in terms of having to price up for capital? On the other hand, the spread has never been wider, from BAA to AAA, which suggests a high degree of risk aversion and that the rates we are seeing are a consistent with a view of who will survive a collapse or a gross estimate / mis-estimate of what the price of credit should look like in advance of the sharpest downturn, possibly, since the data series was collected.

Chart1. Estimated real rates thru 11/19/08., US Corporate Sector (spread shown on RHS axis) THIS YEAR

THIS YEAR

Here is a look at what has happened this year, so one can judge the timing of the rate rise and how much might be attributable to changes in measured inflation not reflected in a fall in nominal rates... (n.b. measured inflation, not inflation expectations, as PK calculated)

Chart 2. Corporate real rates in 2008, with CPI. Spread of BAA to AAA graphed on right axis. I'll update with the expectational variables, if I have the time...

I'll update with the expectational variables, if I have the time...

Is Citigroup under "speculative attack"?

"Discuss amongst yourselves."

There is a fairly strong prima facie case.

It looks like Citibank is ready for its next TARP infusion.

It looks like Citibank is ready for its next TARP infusion.

Meanwhile, Hank "Menace to the Markets" Paulson is hop-scotching in Simi Valley, giving a lecture that, in places, seems to border on a psychotic episode (I have to agree with Cramer about that).

He said, once, he was looking to invest alongside private capital.

Well, he could have seized the day to suggest that Prince Al-Waleed bin Talal's investment was "encouraging" and

"might suggest a way that TARP money can be allocated in the future". The mere suggestion could boost the immediate impact of that investment.

Instead, he misses the opportunity of the day, so that he can what? Lecture to the Reagan faithful about regulation?

It's hard to see why a CMBS portfolio, held for maturity, couldn't be off of mark-to-market.

I'm not sure it will matter, much, for the stock prices, but it will take pressure off the urgency/immediacy surrounding "bank failure", by redefining that term to include an, er... longer-term perspective, right?

Credit spreads currently present a new "conundrum", the word Greenspan once used for an interest rate poser in another context.

Paul Krugman illustrates the latest market conundrum

Paul Krugman illustrates the latest market conundrumEuropean credit spreads were lurching back towards “Armageddon levels” on Wednesday, flirting with their all time highs as speculation mounted over a bail-out for US carmakers. The Markit iTraxx Europe index of investment grade corporate debt widened 12.9 basis points to 175bp, up from a Tuesday closing price of 162bp. The iTraxx Crossover widened by 27.8bp to 899.46, teetering on the brink of the symbolically important 900bp mark last crossed in the fallout after Lehman Brothers collapsed.

THE GRINCH THAT STOLE CHRISTMAS

Labor shedding, widespread. The South is participating, noticeably.

CA's large number looks (to me) like a fluke in this week's read (these big numbers often get reversed in subsequent release).

From the WSJ MarketBeaters blog, on the strangeness of just what 75% VIXy means/implies(!):

...some people have been taking positions in the likes of put options on the S&P at 750. These are expiring at the end of the week and they’re trading at about $3, says William Lefkowitz, chief options strategist at vFinance Investments. A goofy bet like this would normally cost the buyer a nickel, because it’s so preposterous. Not anymore.

FIX THE FORMULA, SAVE THE WORLD

We know that Freddie and Fannie dropped their market share (h/t Krugman) at the time when the worst vintage loans were being originated. Because of Fannie's fancy-accounting penalties and because they did not participate in a lot of the "affordability products" dreamt up, they were not the drivers of the worst excesses of the markets.

What if they had used an "economic underwriting formula", one that was based on economy-wide fundamentals, like median or average household income?

What if they had used an "economic underwriting formula", one that was based on economy-wide fundamentals, like median or average household income?

BUSH, PAULSON, DOLE

They are all out in the past week, bashing the implied government guarantee on trillions of dollars of outstanding agency debt.

George "Little Hoover" Bush at Federal Hall. Paulson yesterday at CEO summit. Elizabeth Dole, lame duck, at today's hearing.

I ... it's so ... astoundingly irresponsible, in the current environment.

They must hate America.

Brad Setser spells out just one of many risk layouts. At a minimum, they hate America's homeowners.

He had time to direct his people to run around and hire money managers and so forth, but according to today's testimony, he's still studying the issue of preventing foreclosures, more than a year after it became consensus that maybe 2 million families were at risk this year alone...

It's not just families at risk. Check it out:

The performance of private label mortgage backed securities that were sliced and diced and sold to investors is just the opposite of Fannie Mae’s and Freddie Mac’s. Private label securities represent less than 20% of the mortgages but 60% of the serious delinquencies. As the regulator of the housing GSEs that own over a quarter of a trillion dollars of private label securities, I ask the private label MBS servicers and investors to rapidly adopt this program as the industry standard. Not only will this streamlined program assist borrowers, but broad acceptance and effective implementation could stabilize communities and property values.

James B. Lockhart, III, Bush Appointee, OFEHO, introducing a new "voluntary program", November 11th

BUYING TIME FOR MONETARY POLICY TO WORK

He has yet to say that a bail-in or bail-out or a "bridge" for GM (or "autos") may be a step in buying time for his monetary policy to work, to 'work through the system'.

To the extent that real economic activity and credit creation (default on a credit report) is being affected by foreclosures, some of which may be "prevented" at the margin (maybe up to 75%, based on IndyMac figures), he hasn't offered an opinion of how that relates to his view of monetary policy, in the short term. (He could use the words "urgent" and "necessary", without stepping outside his lane, right? Greenspan used to cajole and remind legislators of their responsibilities, using all kinds of suasion.)

The conscious step to give the Treasury key responsibility for tough decisions, like who fails and who succeeds, is obvious and understandable. But ... there is more to the big picture than just the necessary liquidity programs, yes?

PPIxF&E - UP, UP, UP

It's an amazing economy, right?

Be careful betting against the U.S. economy, eh?

OMG, WHERE WILL THE BAILOUTS END

Maybe we'll see the end of this meme, today, too. Hewlett Packard appears to have done a good job balancing things ...

FOR NOW, THE LIQUIDITY TRAP IS CANCELED

There will be no 'liquidity trap' with a whopping yield curve like this, perhaps even steeper by today's end:

[yc via bloomberg]

SEE A PENNY, PICK IT UP AND OTHER FALLACIES

If you see a free dollar in a competitive market, do you pick it up or do you say to yourself, "This is too good to be true, there must be a catch"?

Have a look at Mankiw's chart-grab du jour.

According to this chart, unexplained as it is, you'd expect that the UAW would have no trouble organizing workers in foreign manufacturer's plants (God knows, they've tried). What employee wouldn't want very nearly to double their income, their hourly wage?

Since we know that unionization is not spreading quite like that, do you swallow this chart, or ask, "Hey, this can't be true" or "there must be more to the story"?

If you dig into the data, you find out that the author of this chart is intentionally comparing a fully loaded cost with one that isn't (and based on an estimate by Daimler). The comparable wage rate appears to be $47.50 for 2006...

Can I pick on Greg Mankiw for this? He is a well established and deservedly respected economist, who is known for his acumen and thoroughness (that I admire), both of which will endure a pundit on this mini-blog, right?

So here is a query, that I've had in the back of my mind:

When he wrote his letter to POTUS, he advised the new President to keep his economic advisers close, that no one party has "a monopoly" on the truth.

What does that mean, more precisely? Does that mean that Dr. Mankiw believes that he is wrong, 'doesn't have the truth', half the time? I doubt it.

Does it mean that economists use statistics to make "lies of omission", like this chart above, sans explanation? I don't know.

I hope he just means that economists are sometimes prone to offering one side of the story, for the best of motives, so that there is a positive value to having economists with alternative viewpoints "work a problem". But, then, there is this chart above ... hummm.

How did their loan loss reserves get so low? This chart looks like the definition of "FICO madness". Was it all current loss experience, or did somebody decide that the appropriate level of reserves was not much more than what was allowed to count toward Tier 2 capital?

Note to self: credit cards, even at 15% average rate, are not sunflowers that grow to the sky.

Just-in-time loss reservering:

What ever is inside "other loans" and "investments"? Leveraged private equity stuff", commercial real-estate? Synthetic CDOs? (Most of the "Goodwill" is disallowed when calculating capital adequacy).

They have about $100Billion in Tier1 capital and $25 billion in loan reserves, against these assets and all their off balance-sheet exposures. Is it enough? Off hand, it looks too hard to say. It does look unlikely that, on their own, credit cards and RMBS, marked down, would be sufficient to 'break the bank', right?

Something about their jobs cuts and the amount of targeted savings doesn't seem to square, but others know the company better than I do...

I'm so glad that, during a downturn, they can achieve 8% core capital, on the backs of job cuts, with a full guarantee of their debt, and a giant spinnaker-like TARP-sail running with the winds. What is wrong with this picture? More:

We distributed $2.1 billion in dividends to shareholders during the quarter. On October 20, 2008, as previously announced, the Company [the Board of Directors] decreased the quarterly dividend on its common stock to $0.16 per share [about $3.4 billion at an annual rate...]

... of inter-bank freeze. In his testimony, he doesn't address other linkages (derivatives, etc.), sweeping them into 'uncertainty' and parts not central to his basic thesis or description of the contagion.

A large money market fund that had invested in commercial paper issued by Lehman Brothers "broke the buck," i.e., its asset value fell below the dollar amount deposited, breaking an implicit promise that deposits in such funds are totally safe and liquid. This started a run on money market funds and the funds stopped buying commercial paper. Since they were the largest buyers, the commercial paper market ceased to function. The issuers of commercial paper were forced to draw down their credit lines, bringing interbank lending to a standstill. Credit spreads-i.e., the risk premium over and above the riskless rate of interest-widened to unprecedented levels and eventually the stock market was also overwhelmed by panic. All this happened in the space of a week.

Everyone is guilty of it, Left and Right, but when you hear the cause of a problem long before you hear the data, you can bet that something is being shoveled your way.

This happened when we heard how much the Community Reinvestment Act (CRA) was 'the cause', right? Turned out that data was crap. Same for how dangerous it would be if the FDIC limit were not raised to $250,000. Turned out that was crap, too.

Now we hear how bad Freddie and Fannie were, even from the mouth of the President. *sigh*

These two did not participate in the "affordability" products that were dreamt up by the private sector in the first half of the 2000s:

Washington Post Staff Writer

Thursday, May 12, 2005; Page E04

Mortgage financing giant Fannie Mae said yesterday that its share of the mortgage-related securities market dropped from 45 percent in 2003 to 29 percent in 2004 because of the growing popularity of adjustable-rate mortgages, according to a filing with the Securities and Exchange Commission.

An "act of God"?

Financial crises may be an unavoidable aspect of modern capitalism, a consequence of the interactions between hardwired human behavior and the unfettered ability to innovate, compete, and evolve.The quote is a little unfair, he went on to talk about limiting those risks in important ways. Still there are other gems, like government should subsidize geekiness/greekiness (we need to subsidize people who rush out to make, maybe, $220K on Wall Street in their first year?):

-MIT Professor, Andrew Lo. (rest is worth the read)

"In the same way that government grants currently support the majority of Ph.D. programs in science and engineering, new funding should be allocated to major universities to greatly expand degree programs in financial technology."The good guys in the zero-sum game of trading:

Based upon my research on the activities of hedge funds, there are three important findings I would like to share with the Committee. First, hedge funds did not cause the financial crisis and are in fact helping to mitigate its damage and save taxpayers money. This may seem surprising, but in fact hedge funds have historically made markets more stable [!!!] and helped their investors conserve wealth in times of economic stress. Second, hedge funds’ short-selling activities have helped draw attention to the poor management and investment decisions of financial companies in recent years. Indeed, when hedge funds short-sell the stocks of unhealthy companies, they help to divert capital from companies that are fundamentally unstable. This not only prevents stock market bubbles from becoming much worse, but it helps to ensure that companies that make sound decisions are rewarded and are able to provide stable jobs for their employees. Finally, existing laws and regulations should be strictly enforced against hedge funds and their managers, but changing how hedge funds are regulated could actually undermine the interests of investors and increase economic instability.

-Houman Shadab, Senior Research Fellow, Mercatus Center, George Mason University

Moody’s raising its expectations (again) that corporate default rates will rise, i.e. higher corporate defaults and even further pressures on CDSs and synthetic CDOs - FT Alphaville

The weekly claims are out.

Scanning the reports for the past four or five weeks, there are signs that California and Florida may be bottoming a tad, just as the "rust belt" is ramping up big time. Michigan and Ohio (and Pennsylvania) have been hit hard, at the margin, in the past weeks. Autos and manufacturing.

This is rather mercenary, but ...

Notice that the non-pension post-retirement benefits of $33 billion equate to $55/share?

If the UAW and "The Government" can come to an understanding, that's a whole LOT of bargaining power.

So much that you could buy out the existing stock holders (just $2 billion), pay off the debholders at market prices, whip this puppy through bankruptcy, maybe, to get out from dealer contracts and the onerous aspects of Cerberus agreement, and still turn a very significant cash profit, in the short-term.

So many have stopped listening, long ago, perhaps, but that doesn't mean it isn't still important.

So many have stopped listening, long ago, perhaps, but that doesn't mean it isn't still important.

I've pulled some stuff from their 2007 Annual Report, to outline what the company thinks is going on. The details on the VEBA cash funding ... well, it appears that is down the road, truly (as of this writing). At least, it's doesn't look as though it was pre-funded in 2007 or that they are doing more than accrual for it, presently. At least in the current period, the UAW has agreed to them deferring $1.7B of interim cash payments to the VEBA.

Still, you get the general direction, and maybe some inklings on how to assess their own assessment.

Among noteworthy items:

| 2008 | 2009-2010 | 2011-2012 | 2013 and after | Total | ||||||||||||||||

| (Dollars in millions) | ||||||||||||||||||||

| Postretirement benefits (a)(b) | $ | 3,338 | $ | 6,802 | $ | 4,814 | $ | — | $ | 14,954 | ||||||||||

| Less: VEBA assets (a) | (3,338 | ) | (6,802 | ) | (4,814 | ) | — | (14,954 | ) | |||||||||||

| Net postretirement benefits | — | — | — | — | — | |||||||||||||||

| Net increases due to finalization of the Settlement Agreement | — | — | 7,590 | 12,015 | 19,605 | |||||||||||||||

| Total | $ | — | $ | — | $ | 7,590 | $ | 12,015 | $ | 19,605 | ||||||||||

| Remaining balance postretirement benefits (a) | $ | 728 | $ | 1,772 | $ | 5,248 | $ | 41,311 | $ | 49,059 | ||||||||||

| Less: VEBA assets (a) | (728 | ) | (621 | ) | — | — | (1,349 | ) | ||||||||||||

| Net | — | 1,151 | 5,248 | 41,311 | 47,710 | |||||||||||||||

| Net increases (decreases) due to finalization of the Settlement Agreement | 165 | (246 | ) | (3,636 | ) | (29,286 | ) | (33,003 | ) | |||||||||||

| Total | $ | 165 | $ | 905 | $ | 1,612 | $ | 12,025 | $ | 14,707 | ||||||||||

| (a) | As reported in our 2007 10-K prior to the finalization of the Settlement Agreement. | |

| (b) | Amounts include postretirement benefits under the current contractual labor agreements in North America. The remainder of the estimated liability for benefits beyond the current labor agreement and for essentially all salaried employees, is classified under remaining balance of postretirement benefits. These obligations are not contractual. |

| • | Salaried employment savings (estimated $1.5 billion effect) — We are executing salaried headcount reductions in the U.S. and Canada through normal attrition, early retirements, mutual separation programs and other tools. In September 2008, we extended voluntary early retirement offers under our Salaried Retirement Window Program (Salaried Window Program) to certain of our U.S. salaried employees. Employees accepting the Salaried Retirement Window Program were required to do so no later than October 24, 2008, with the majority of retirements taking place on November 1, 2008. As of October 31, 2008, 3,460 employees had irrevocably accepted the Salaried Retirement Window Program, which was in excess of the 3,000 needed to achieve our financial target. In addition, health care coverage for U.S. salaried retirees over 65 has been eliminated, effective January 1, 2009. Furthermore, there will be no new base compensation increases for U.S. and Canadian salaried employees for the remainder of 2008 and 2009. We are also eliminating discretionary cash bonuses for the executive group in 2008. | |||

| • | GMNA structural cost reductions (estimated $2.5 billion effect) — Significant progress has been made towards achieving GMNA’s structural cost reduction target. We have accelerated cessation of production at two assembly facilities in addition to shift and line-rate reductions at other facilities. Truck capacity is expected to be reduced by 300,000 vehicles by the end of 2009. Promotional and advertising spending is being reduced by 25% and 20%, respectively, and engineering spending is being curtailed as well. In addition, we are implementing significant reductions in discretionary spending (e.g., travel, non-core information technology projects and consulting services). | |||

| • | Capital expenditure reductions (estimated $1.5 billion effect) — The major components of this reduction are related to a delay in the next generation large pick-up truck and sport utility vehicle programs, as well as V-8 engine development. There will also be reductions in non-product capital spending. These reductions will be partially offset by increases in powertrain spending related to alternative propulsion, small displacement engines and fuel economy technologies. | |||

| • | Working capital improvements (estimated $2.0 billion effect) — Actions are being taken to improve working capital by approximately $1.5 billion in North America and $0.5 billion in Europe by December 31, 2009, primarily by reducing raw material, work-in-progress and finished goods inventory levels as well as implementing lean inventory practices at parts warehouses. All these initiatives are on track for completion prior to December 31, 2009. | |||

| • | UAW VEBA payment deferrals (estimated $1.7 billion effect) — Approximately $1.7 billion of payments that had been scheduled to be made to a temporary asset account in 2008 and 2009 for the establishment of the New VEBA has been deferred until 2010. The outstanding payable resulting from this deferral will accrue interest at 9% per annum. The UAW and Class Counsel have agreed that this deferral will not constitute a change in or breach of the Settlement Agreement. Within 20 business days of the Implementation Date, approximately $7.0 billion of deferred payments, plus interest plus additional contractual amounts will be due to the New VEBA. |

| • | Asset sales — We are exploring the sale of the HUMMER business, Strasbourg transmission plant and the AC Delco business. We expect to shortly commence providing offering materials to potential buyers for the HUMMER and AC Delco businesses pursuant to appropriate confidentiality agreements and have already commenced providing confidential offering materials for the Strasbourg transmission plant to interested parties. We are also in the process of monetizing idle or excess real estate and several individual transactions are in various stages of execution. | |

| • | Capital market activities — Our plan targeted at least $2.0 billion to $3.0 billion of financing during 2008 and 2009. However, due to the prevailing global economic conditions and our current financial condition and near-term outlook, we currently do not have access to the capital markets on acceptable terms. In the three months ended September 30, 2008, we executed $0.5 billion of debt-for-equity exchanges of our Series D convertible bonds due in June 2009. In addition, we have gross unencumbered assets of over $20 billion, which could support a secured debt offering, or multiple offerings, in excess of the initially targeted $2.0 billion to $3.0 billion, if market conditions recover. These assets include stock of foreign subsidiaries, brands, our investment in GMAC and real estate. |

| • | Salaried employment savings (estimated $0.5 billion effect) — Additional salaried employment savings will be achieved through incremental workforce reductions in U.S. and Canada, including involuntary separation initiatives. In addition, we have announced the suspension of our matching contribution to certain defined contribution plans starting November 1, 2008 as well as suspension of other reimbursement programs for U.S. and Canadian salaried employees. We also expect to realize salaried employment savings in Western Europe in 2009 through a wage/salary freeze and other cost reduction initiatives. | |

| • | Additional GMNA structural cost reductions (estimated $1.5 billion effect) — We expect to reduce GMNA structural cost by an additional $1.5 billion in 2009. These additional reductions would result from the recently announced acceleration of previously planned capacity actions and other plant operating plan changes, additional efficiencies in engineering resources aligned with further product plan changes, continued marketing spending reductions aligned with expected automotive industry conditions and intensified focus on discretionary spending reductions. | |

| • | Additional working capital reductions (estimated $0.5 billion effect) — GMNA is targeting approximately $0.5 billion of additional working capital reductions beyond the original 2008 target reduction level of $1.5 billion. This additional target reduction is expected to be achieved by continuing to focus on inventory reductions and initiatives related to accounts payable. | |

| • | Additional capital expenditure reductions (estimated $2.5 billion effect) — In the absence of federal funding support, 2009 capital spending will be reduced from the revised target of $7.2 billion announced on July 15 to $4.8 billion. This reduction will be achieved primarily through deferrals of selected programs (e.g., the Cadillac CTS coupe and the next generation Chevy Aveo for the global market) and related capacity reduction projects. However, we are still planning to increase global spending for fuel economy improvements, and spending related to the Chevy Volt will continue. Beyond 2009, capital expenditures will stabilize in the $6.5 billion to $7.0 billion range (excluding China, which is self funded with our joint venture partner). |

{kind=link}